Buying equipment based on purchase price alone is one of the most expensive mistakes in engineering procurement — the sticker price is often the smallest part of what you'll actually spend. Use this Life Cycle Cost Ownership Calculator to calculate total cost of ownership using acquisition cost, operating expenses, maintenance, energy consumption, downtime, and disposal value across the full service life. It matters across manufacturing, infrastructure, fleet management, and facilities — anywhere a capital investment runs for years and accumulates costs well beyond the initial invoice. This page includes the LCC formula, a worked HVAC example, NPV and break-even theory, and a full FAQ.

What is Life Cycle Cost?

Life cycle cost (LCC) is the total amount you spend on a piece of equipment or system from the day you buy it to the day you dispose of it. It adds up every dollar — purchase price, installation, energy, maintenance, downtime, and end-of-life costs — so you can compare options on what they actually cost, not just what they cost upfront.

Simple Explanation

Think of it like buying a car: the cheapest car on the lot might cost you far more over 10 years in fuel, repairs, and breakdowns than a pricier, more reliable model. LCC works the same way for industrial equipment — it looks at the full picture over the entire lifespan, not just the purchase price. The goal is to find the option that costs least in total, not least today.

📐 Browse all 1000+ Interactive Calculators

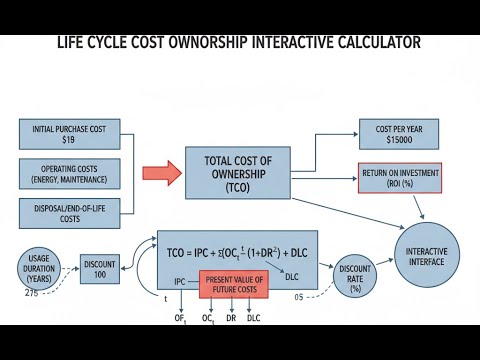

Visual Diagram: Life Cycle Cost Components

Life Cycle Cost Ownership Calculator

How to Use This Calculator

- Select your calculation mode — Total Life Cycle Cost, NPV Analysis, Compare Two Options, Break-Even, or Annual Equivalent Cost.

- Enter the relevant cost inputs for your selected mode (purchase cost, installation, annual operating costs, energy, maintenance, downtime, service life, discount rate, and/or salvage value as applicable).

- Adjust the service life and discount rate to match your project's actual horizon and financing context.

- Click Calculate to see your result.

Life cycle cost ownership interactive visualizer

Compare equipment options across their full service life, not just purchase price. Watch how small differences in operating costs compound to massive totals over years.

TOTAL LCC

$215,000

OPERATING %

77%

ANNUAL COST

$14,333

FIRGELLI Automations — Interactive Engineering Calculators

Formulas & Life Cycle Cost Equations

Use the formula below to calculate total life cycle cost.

Total Life Cycle Cost

LCC = CI + Cinst + Σ(CO + CM + CE + CD) + Cdisp

CI = Initial purchase cost ($)

Cinst = Installation cost ($)

CO = Annual operating cost ($/year)

CM = Annual maintenance cost ($/year)

CE = Annual energy cost ($/year)

CD = Annual downtime cost ($/year)

Cdisp = Disposal cost minus salvage value ($)

Σ = Summation over service life

Use the formula below to calculate net present value.

Net Present Value

NPV = -C0 + Σ[CFt / (1 + r)t] + S / (1 + r)n

C0 = Initial investment ($)

CFt = Cash flow in year t ($/year)

r = Discount rate (decimal)

t = Year number (1, 2, 3, ... n)

S = Salvage value ($)

n = Project life (years)

Use the formula below to calculate annual equivalent cost.

Annual Equivalent Cost

AEC = LCC × CRF = LCC × [r(1 + r)n] / [(1 + r)n - 1]

AEC = Annual equivalent cost ($/year)

LCC = Total life cycle cost ($)

CRF = Capital recovery factor (dimensionless)

r = Discount rate (decimal)

n = Service life (years)

Use the formula below to calculate break-even period.

Break-Even Period

TBE = ΔCinitial / ΔCannual

TBE = Break-even time (years)

ΔCinitial = Difference in initial costs ($)

ΔCannual = Difference in annual operating costs ($/year)

Simple Example

Equipment A costs $20,000 to purchase, $1,000 to install, and $3,000/year to run (operating + maintenance + energy) over a 5-year service life with $500 salvage value at end of life.

LCC = ($20,000 + $1,000) + ($3,000 × 5) − $500 = $21,000 + $15,000 − $500 = $35,500

Annualized cost = $35,500 ÷ 5 = $7,100/year

Theory & Engineering Applications of Life Cycle Costing

Life cycle cost analysis represents a comprehensive economic evaluation methodology that extends far beyond simple acquisition price comparison. Engineering decisions made during procurement affect operational expenses, maintenance requirements, energy consumption, and disposal costs for decades. A manufacturing facility purchasing a $100,000 compressor system with 85% energy efficiency versus a $140,000 unit at 93% efficiency demonstrates this principle — over a 20-year service life operating 6,000 hours annually at $0.12/kWh for a 75 kW motor, the higher-efficiency unit saves approximately $108,000 in energy costs alone, making it the economical choice despite the 40% higher purchase price.

Time Value of Money and Discount Rate Selection

The discount rate fundamentally transforms LCC analysis from simple arithmetic to sophisticated financial modeling. This rate reflects opportunity cost, inflation, and risk, converting future expenditures to present value equivalents. Federal agencies typically use 3-7% discount rates for public infrastructure, while private corporations may apply 10-15% rates reflecting shareholder return expectations and capital costs. The choice profoundly impacts decision-making: at 3% discount, a $50,000 expense 15 years hence has a present value of $32,076, but at 10% it drops to $11,970.

This explains why high discount rates favor lower initial costs with higher operating expenses — future costs become heavily discounted. Defense procurement often uses lower rates (2-4%) because assets serve national security over 30-50 year horizons, while technology equipment uses higher rates (12-18%) reflecting rapid obsolescence and 3-5 year replacement cycles.

Hidden Cost Categories in Industrial Systems

Downtime costs frequently exceed all other operating expenses in production environments yet remain poorly quantified in many LCC analyses. A pharmaceutical filling line generating $18,000 per hour in finished product value experiences true downtime costs of $18,000/hour plus labor, material waste, and schedule disruption — often totaling $25,000-$30,000 per hour. Reliability-centered maintenance principles suggest that equipment with 99.2% availability versus 97.5% availability operating 8,760 hours annually creates 149 hours versus 219 hours of downtime — a 70-hour differential.

At $25,000/hour, this represents $1.75 million in annual value difference, justifying substantial initial cost premiums for higher-reliability equipment. This calculation method applies across automotive assembly, semiconductor fabrication, and food processing where line stoppages cascade through integrated production systems.

Energy Cost Escalation and Long-Term Projections

Historical energy price volatility introduces significant uncertainty into LCC calculations for energy-intensive equipment. U.S. industrial electricity prices increased from $0.0483/kWh in 2000 to $0.0712/kWh in 2023 — a 47% rise over 23 years, or approximately 1.7% annual escalation above inflation. Conservative LCC analyses incorporate energy escalation rates of 2-3% annually above the general discount rate. For a data center consuming 2.5 MW continuously, the difference between flat energy costs and 2.5% annual escalation over 15 years equals $8.7 million in additional expenses (assuming $0.08/kWh baseline).

Variable frequency drives, high-efficiency motors, heat recovery systems, and LED lighting retrofits all demonstrate enhanced economic justification when energy escalation factors enter the analysis. Process industries performing LCC analysis should separate energy costs from other operating expenses and apply sector-specific escalation rates based on fuel type — natural gas, electricity, or diesel — each following distinct price trajectories.

Worked Example: HVAC System Selection for Commercial Building

A 150,000 square foot office building in Chicago requires HVAC replacement. Two systems warrant evaluation:

Option A: Standard Efficiency System

Initial equipment cost: $385,000

Installation cost: $95,000

Annual energy consumption: 1,850,000 kWh at $0.095/kWh = $175,750/year

Annual maintenance: $18,500

Service life: 18 years

Salvage value: $12,000

Option B: High Efficiency System with Heat Recovery

Initial equipment cost: $565,000

Installation cost: $115,000

Annual energy consumption: 1,295,000 kWh at $0.095/kWh = $123,025/year

Annual maintenance: $24,750

Service life: 22 years

Salvage value: $28,000

Using 5% discount rate and 2% annual energy cost escalation, we calculate NPV for each option over an 18-year common analysis period (Option A's full life):

Option A Calculations:

Initial costs: $385,000 + $95,000 = $480,000

Year 1 operating cost: $175,750 + $18,500 = $194,250

Year 2 operating cost: ($175,750 × 1.02) + $18,500 = $197,758

Continuing this pattern through year 18, then discounting each year's cost to present value using the formula: PV = Cost / (1.05)year

Summing all present values:

PV of operating costs (years 1-18): $2,847,365

PV of salvage value: $12,000 / (1.05)18 = $4,992

Total LCC (Option A): $480,000 + $2,847,365 - $4,992 = $3,322,373

Option B Calculations:

Initial costs: $565,000 + $115,000 = $680,000

Year 1 operating cost: $123,025 + $24,750 = $147,775

Year 2 operating cost: ($123,025 × 1.02) + $24,750 = $150,236

Following the same discounting methodology through year 18:

PV of operating costs (years 1-18): $2,174,483

Total LCC (Option B, 18-year analysis): $680,000 + $2,174,483 = $2,854,483

Economic Comparison:

Net savings with Option B: $3,322,373 - $2,854,483 = $467,890

Savings as percentage: 14.1% over analysis period

Simple payback period: ($680,000 - $480,000) / ($194,250 - $147,775) = 4.3 years

Discounted payback: Approximately 5.1 years (accounting for time value)

This analysis reveals that despite a $200,000 higher initial investment (41.7% premium), Option B delivers nearly $468,000 in present value savings over 18 years. The energy savings of $52,725/year in year one, escalating at 2% annually, compound to create overwhelming economic advantage. Additionally, Option B's 22-year service life versus 18 years provides four additional years of service value not captured in this conservative 18-year analysis window.

Maintenance Cost Modeling and Equipment Aging

Constant annual maintenance costs represent an oversimplification in most LCC models. Real-world maintenance expenses follow escalating patterns as equipment ages — hydraulic systems develop seal leaks, bearings wear, control systems require reprogramming, and component obsolescence forces expensive retrofits. A realistic maintenance cost model uses a bathtub curve with three phases: early life (infant mortality), stable operation, and wear-out period. Industrial pumps typically show stable maintenance years 3-10, then 8-12% annual cost increases through year 20.

A pump with $4,000 annual maintenance years 3-10 might require $4,320 in year 11, $4,666 in year 12, escalating to $8,200 by year 20. Incorporating this realistic cost progression into LCC analysis increases total costs by 15-22% compared to flat-rate models, favoring equipment replacement at optimal economic life rather than running assets to failure.

Sensitivity Analysis and Monte Carlo Simulation

LCC calculations contain multiple uncertain variables — discount rates, energy prices, maintenance costs, equipment lifespans, and utilization rates — each affecting outcomes. Deterministic single-point estimates mask this uncertainty. Sophisticated LCC analysis employs sensitivity analysis, varying each parameter individually to identify which variables most impact decision-making. A tornado diagram ranks parameters by influence magnitude.

For major capital decisions, Monte Carlo simulation runs 10,000+ iterations with probability distributions for each variable, generating a distribution of possible LCC outcomes rather than single values. This reveals that "Option A: $2.85M" might actually represent a 90% confidence interval of $2.31M to $3.67M, while "Option B: $3.22M" spans $2.89M to $3.58M — potentially reversing the decision when uncertainty is properly quantified. Risk-averse organizations might select the option with lower worst-case outcome even if mean costs are higher.

For those performing comparative economic analysis across multiple options, the engineering calculator library offers additional tools for payback period calculation, internal rate of return, and benefit-cost ratio analysis that complement LCC methodology.

Practical Applications

Scenario: Fleet Manager Evaluating Electric Delivery Vans

Marcus oversees a logistics company operating 120 delivery vans across metropolitan Atlanta, facing replacement decisions for aging diesel vehicles. He compares conventional diesel vans at $42,000 each against electric vehicles at $58,000. Using the Life Cycle Cost calculator's comparison mode, Marcus inputs diesel fuel costs of $8,400/year versus electric charging costs of $2,100/year, plus diesel maintenance averaging $3,200/year versus EV maintenance at $1,400/year. The calculator reveals that over the typical 8-year fleet service life with a 4.5% discount rate, electric vans deliver total lifecycle costs of $78,350 versus $94,680 for diesel—a $16,330 savings per vehicle, or nearly $2 million fleet-wide. This analysis secured board approval for EV transition despite the higher purchase price, transforming the company's environmental footprint while improving bottom-line economics.

Scenario: Manufacturing Engineer Justifying Automation Investment

Jennifer manages production operations at a medical device manufacturer considering a $475,000 automated inspection system to replace manual quality control processes costing $185,000 annually in labor and $28,000 in scrap/rework. She uses the NPV calculator mode to evaluate the investment over 12 years with her company's 8% hurdle rate, entering the automation system's $42,000 annual maintenance cost and $18,000 energy expense. The calculator shows an NPV of $687,450, strongly positive, with the annual savings of $153,000 creating compelling justification. Jennifer presents these results to finance leadership, demonstrating that the automation pays for itself in 3.1 years while delivering over $1.16 million in cumulative savings through year 12. The data-driven LCC analysis overcame initial resistance to the capital expenditure, leading to project approval and subsequent 40% reduction in quality escapes.

Scenario: Facilities Director Selecting Roofing System

David manages facilities for a 450,000 square foot distribution center requiring roof replacement. A contractor proposes a standard EPDM rubber membrane at $1.8 million with 15-year warranty versus a premium TPO cool-roof system at $2.35 million with 25-year warranty and superior reflectivity reducing cooling loads. Using the break-even calculator, David inputs the $550,000 cost difference against estimated cooling savings of $47,000/year from reduced heat island effect and lower HVAC demand. The calculator determines a break-even period of 11.7 years, meaning the premium roofing system pays for itself before the standard roof even reaches its warranty limit. By year 25, cumulative savings exceed $625,000 while avoiding a mid-life replacement. This LCC analysis convinced executive leadership to approve the higher initial investment, recognizing that lifecycle economics decisively favor the premium solution despite budget pressures favoring lower upfront costs.

Frequently Asked Questions

Free Engineering Calculators

Explore our complete library of free engineering and physics calculators.

Browse All Calculators →🔗 Explore More Free Engineering Calculators

About the Author

Robbie Dickson — Chief Engineer & Founder, FIRGELLI Automations

Robbie Dickson brings over two decades of engineering expertise to FIRGELLI Automations. With a distinguished career at Rolls-Royce, BMW, and Ford, he has deep expertise in mechanical systems, actuator technology, and precision engineering.

Need to implement these calculations?

Explore the precision-engineered motion control solutions used by top engineers.