When you're putting equipment or a project on finance, your monthly payment is only part of the story. Most people focus on what leaves the account each month, but it's the full principal and interest breakdown that determines your actual long-term costs. This loan amortization schedule calculator lets you see how much you’ll pay each month, your total interest, and exactly how each payment chips away at your original loan. In manufacturing, plant upgrades, or major project management, understanding where your money is going will tell you if the financing is sensible. Below you'll find the working formulas, a walkthrough example, some engineering background, and a straight FAQ.

What is a Loan Amortization Schedule?

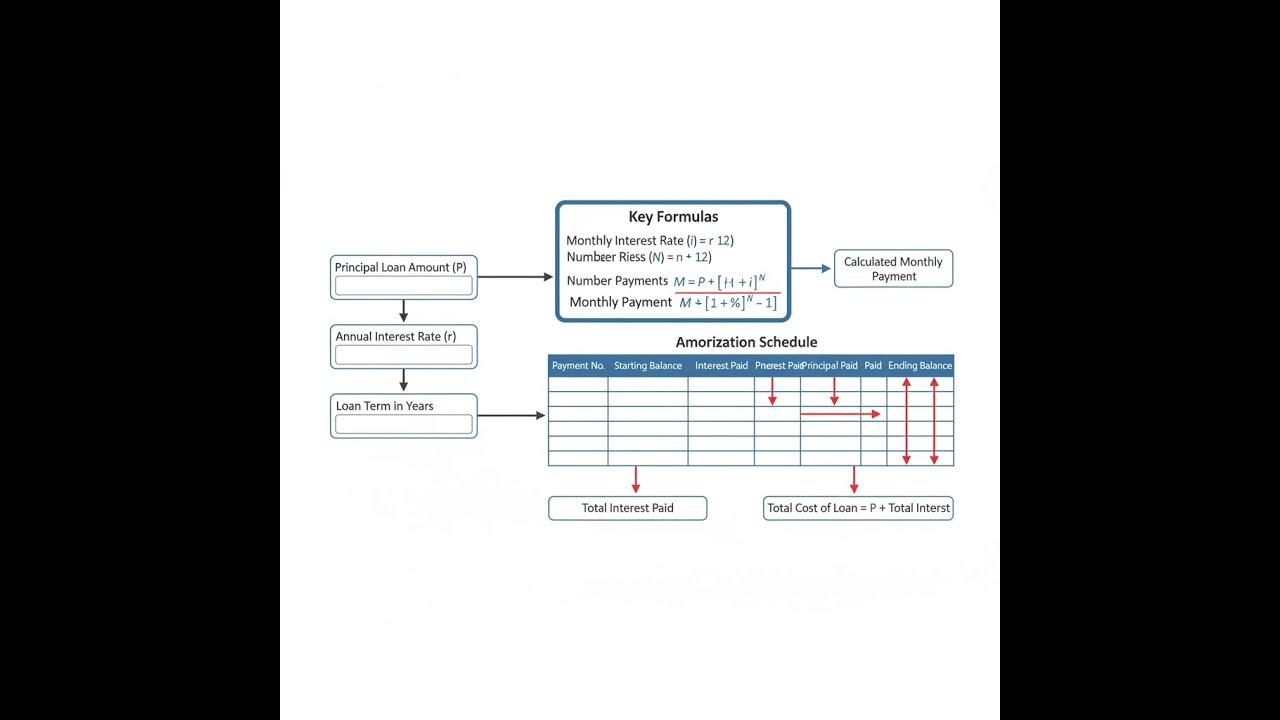

A loan amortization schedule is a list showing how each payment on a loan is split between paying down principal and paying interest to the lender. It tracks the gradual reduction of what you owe from start to finish, period by period.

Simple Explanation

An amortization schedule works a bit like gradually eating a big meal: each payment is a bite, but at first, most of that bite goes to interest. You barely make a dent in the main debt. As time passes and the balance drops, the interest charge on each payment shrinks, so more of your money starts bringing down the debt faster.

📐 Browse all 1000+ Interactive Calculators

Diagram

Loan Amortization Schedule Calculator

How to Use This Calculator

This calculator is intended for education, concept evaluation, and preliminary design. Results are based on the equations and assumptions described on this page, but cannot account for every real-world load case, tolerance, material property, environmental condition, installation detail, safety factor, code, or regulatory requirement. Verify all inputs, assumptions, units, and results independently before selecting components or using the result in a real application. Safety-critical, structural, medical, lifting, transportation, or regulated applications must be reviewed by a qualified engineer.

- Choose your Calculation Mode—you can see a full schedule, monthly payment, principal, rate, term, or see the impact of early payoff.

- Fill in the Loan Amount, Annual Interest Rate (%), and Loan Term (Years)—or just the fields related to your chosen mode.

- Put in the Loan Start Date if you want the schedule to match your expected start.

- Hit Calculate. Your answer will show up below.

Loan Amortization Schedule Interactive Visualizer

You can see from the graph just how the split between principal and interest changes over the life of the loan. At first, most of your payment goes to interest; over time, more goes to principal.

Monthly Payment

$1,688

Total Interest

$103,788

Total Cost

$303,788

FIRGELLI Automations — Interactive Engineering Calculators

Equations & Formulas

To determine your monthly payment for a standard amortized loan, you use the following formula. It takes your principal, annual interest (divided by 12 to get monthly), and the total number of payments over the loan.

Monthly Payment Formula

M = P × [r(1 + r)n] / [(1 + r)n - 1]

Where:

M = Monthly payment ($)

P = Principal loan amount ($)

r = Monthly interest rate (annual rate ÷ 12 ÷ 100)

n = Total number of payments (years × 12)

To isolate how much of a single payment goes to interest, use:

Interest Payment for Period t

It = Bt-1 × r

Where:

It = Interest payment in period t ($)

Bt-1 = Outstanding balance at beginning of period t ($)

r = Monthly interest rate

To find the principal paid in a single period, subtract the interest portion from the fixed monthly payment:

Principal Payment for Period t

PRt = M - It

Where:

PRt = Principal payment in period t ($)

M = Monthly payment ($)

It = Interest payment in period t ($)

To update the outstanding balance after each payment, simply subtract the principal component from the prior balance:

Remaining Balance After Payment t

Bt = Bt-1 - PRt

Where:

Bt = Outstanding balance after payment t ($)

Bt-1 = Outstanding balance before payment t ($)

PRt = Principal payment in period t ($)

For the total interest paid over the life of the loan, use this formula:

Total Interest Paid

Total Interest = (M × n) - P

Where:

M = Monthly payment ($)

n = Total number of payments

P = Original principal ($)

Simple Example

Suppose you borrow $100,000 at 6% for 10 years (120 payments).

Monthly rate r = 6% ÷ 12 ÷ 100 = 0.005. Monthly payment M = $1,110.21.

First month: interest = $100,000 × 0.005 = $500.00; principal paid = $1,110.21 − $500.00 = $610.21. Balance = $99,389.79.

Total paid over the 10 years = $133,224.60. Interest paid = $33,224.60.

Theory & Engineering Applications

Amortization is simply chipping away at a loan in fixed payments, each covering some principal plus interest. With amortized loans, as you pay down the principal, the interest charged each period drops because it’s always calculated off the outstanding balance. This differs from simple interest loans, which charge interest only on the original amount, regardless of how much you’ve paid.

Mathematical Foundation of Amortization

The core amortization formula is just the present value of a series of equal payments (an annuity) discounted back with the periodic interest rate. Each payment is worth less the further out it is, so the formula scales your fixed monthly payment so a series of them will pay off the starting balance to the penny over n months. Even a small difference in interest rate changes the total interest sharply—just a half-percent higher rate on a 30-year, $250,000 loan adds about $28,500 in interest. Your focus during negotiations should be the real rate, not just the payment.

Engineering Economics and Capital Equipment Financing

For engineers calculating the viability of financing production lines, buildings, or capital projects, amortization schedules deliver the real long-term cost—not just the cash flow today. Every project NPV or IRR analysis should use the actual payment schedules, because the timing and amount of each outflow shapes feasibility. For example, a $2M robot line at 7.25% over 10 years means $23,476.89 per month, and you pay $817,227.27 just in interest before you own the asset. This is only worthwhile if the benefits (productivity, labor savings, alternate investment returns) outstrip the financing cost.

Tax Implications and Deductibility

The reason to track principal and interest separately is because one is potentially deductible, the other isn’t. Businesses write off interest as an expense, but not principal—this matters for true after-tax borrowing costs. For example, if a company can deduct 21% in tax, a 6.5% loan costs 5.135% after taxes. Month-by-month, the actual interest portion shown on the amortization schedule is what gets reported, so accuracy here saves on paperwork headaches later. If your reporting doesn’t align with the payment dates, you need the full schedule to split interest correctly across fiscal periods.

Worked Example: Industrial Equipment Purchase Analysis

Scenario: You’re a manufacturing business financing a $485,000 CNC machine at 7.8% over 7 years. The equipment should generate $9,500/month. You need to see the whole payment structure and when the purchase pays for itself.

Given Data:

- Principal amount (P) = $485,000

- Annual interest rate = 7.8%

- Loan term = 7 years = 84 months

- Expected monthly revenue = $9,500

Step 1: Monthly interest rate

r = 7.8% ÷ 12 ÷ 100 = 0.0065

Step 2: Monthly payment with the formula

M = P × [r(1 + r)ⁿ] / [(1 + r)ⁿ - 1]

M = 485,000 × [0.0065(1.0065)⁸⁴] / [(1.0065)⁸⁴ - 1]

M = 485,000 × [0.0065 × 1.7287] / [1.7287 - 1]

M = 485,000 × [0.011237] / [0.7287]

M = 485,000 × 0.015420

M = $7,478.87 per month

Step 3: What’s interest and what’s principal in payment #1

Interest (first payment): I₁ = $485,000 × 0.0065 = $3,152.50

Principal: PR₁ = $7,478.87 - $3,152.50 = $4,326.37

Remaining balance: B₁ = $485,000 - $4,326.37 = $480,673.63

Step 4: Total lifetime cost

Total payments = $7,478.87 × 84 = $628,225.08

Total interest paid = $628,225.08 - $485,000 = $143,225.08

Interest as percent of principal = ($143,225.08 ÷ $485,000) × 100 = 29.5%

Step 5: Cash flow impact

Net monthly cash flow = $9,500 - $7,478.87 = $2,021.13 surplus

This confirms loan payments are manageable relative to revenue from day one.

Step 6: Payment breakdown at month 42 (halfway point)

Need remaining balance after 41 payments. Formula:

B₄₁ = P × [(1+r)ⁿ - (1+r)ᵗ] / [(1+r)ⁿ - 1]

B₄₁ = 485,000 × [(1.0065)⁸⁴ - (1.0065)⁴¹] / [(1.0065)⁸⁴ - 1]

B₄₁ = 485,000 × [1.7287 - 1.3087] / [0.7287]

B₄₁ = 485,000 × 0.5762 = $279,456.70

Interest for this payment: I₄₂ = $279,456.70 × 0.0065 = $1,816.47

Principal for this payment: PR₄₂ = $7,478.87 - $1,816.47 = $5,662.40

Over time, more of your payment is going to principal—the schedule lets you see exactly how the savings accelerate later in the loan.

Step 7: Engineering comparison

The cost of interest (29.5% here) should be weighed against options—another lender, using cash, or alternative investments. If your internal cost of capital is higher than the loan rate, borrowing may be better. Use the full amortization table to calculate real NPV, not just "rules of thumb."

Details matter: the payment structure affects tax write-offs, potential refinancing, and return on investment. Using full schedules is standard in engineering budgeting.

Early Payoff Strategies and Prepayment Impact

Extra payments toward principal slice straight into the core loan balance and reduce the total interest owed. Early extra payments save the most in interest, because they reduce the base amount before most of the interest gets calculated. For example, with a $7,478.87 monthly payment, an added $500 each month pays the loan off about 13 months early and saves you around $18,200 in interest—your rate of return on that prepayment is the same as the loan’s rate, which is tough to match elsewhere for guaranteed results.

Practical Applications

Scenario: Manufacturing Facility Expansion Decision

James, heading up facilities at a car parts plant, plans a $1.2 million install for a new automated paint line, financed at 8.5% over 10 years. He checks the amortization calculator and sees a monthly payment of $14,863.58, with $583,629.81 in total interest—close to half the cost of the machine. Looking at the breakdown, year one alone has $96,847 to interest, $81,515 to principal. That full view makes it clear to management that reducing the loan (with a higher down payment) saves serious money: going to $900,000 financed cuts their monthly to $11,147.69 and total interest by over $146,000. They use the full schedule in budget talks, not just the monthly payment.

Scenario: Engineering Firm Office Building Purchase

Maria, financial chief at a mid-sized civil engineering firm, compares buying their building for $875,000 (at 6.75% for 25 years) to leasing at $8,200 per month. The scheduled payment would be $6,233.82—less than rent. But her amortization schedule shows in year one, $58,239 is just interest (and only $16,566 toward principal). For tax paperwork, these splits are needed since only interest is deductible. After 5 years, they’d still owe $810,447. Maria also tries a calculation with a $1,000 monthly prepayment, showing they’d pay off the loan in 18.3 years instead of 25, saving $164,832 in interest. These details are what prompt smart decisions, not just comparing the monthly checks.

Scenario: Research Equipment Financing for University Lab

Dr. Chen, an engineering professor, gets a $650,000 grant for a test lab. University procurement suggests using 5.25% financing over 5 years to stretch grant dollars for other lab needs. Monthly payment: $12,301.74. Total interest: $88,104.55. Since grants can cover certain interest types, Dr. Chen uses the full amortization schedule to show $2,843.75 of the first payment is interest. Tracking this monthly lets the lab team match expenses to the university’s fiscal calendar, aligning real costs with budgeting and reporting. The full table lays out exactly what’s due, when, and what portion qualifies for grant coverage or reporting.

Frequently Asked Questions

▼ Why does most of my payment go to interest in the early years?

▼ How much can I really save by making extra principal payments?

▼ Should I use extra cash to pay down my loan or invest it elsewhere?

▼ What's the difference between amortization and simple interest loans?

▼ How do I use an amortization schedule for tax reporting?

▼ Can I calculate the interest rate if I only know the payment amount?

Free Engineering Calculators

Explore our complete library of free engineering and physics calculators.

Browse All Calculators →🔗 Explore More Free Engineering Calculators

About the Author

Robbie Dickson — Chief Engineer & Founder, FIRGELLI Automations

Robbie Dickson brings over two decades of engineering expertise to FIRGELLI Automations. With a distinguished career at Rolls-Royce, BMW, and Ford, he has deep expertise in mechanical systems, actuator technology, and precision engineering.

Video Walkthrough - How to Use This Calculator

Need to implement these calculations?

Explore the precision-engineered motion control solutions used by top engineers.