Pricing a manufactured product without accurate overhead allocation is a fast path to quoting yourself out of profit. Every indirect factory cost—utilities, depreciation, maintenance, quality control, supervision—has to land somewhere on your cost sheet, and that's exactly what this calculator handles. Use this Manufacturing Cost Overhead Calculator to calculate overhead rates, total manufacturing cost, and unit cost using direct materials, direct labor, overhead totals, and production volume. Getting this right matters in contract manufacturing, medical device production, aerospace fabrication, and custom fabrication shops where margins are tight and underapplied overhead kills profitability. This page includes the core formulas, a worked example, allocation theory, and a full FAQ.

What is Manufacturing Overhead?

Manufacturing overhead is every indirect factory cost that isn't direct materials or direct labor — things like equipment depreciation, utilities, maintenance, and quality control salaries. These costs are real, but they can't be traced to a single product directly, so you allocate them systematically across your production output.

Simple Explanation

Think of overhead like the rent on a shared workshop — everyone using the space has to chip in, even if they don't use every corner of it. The more of the shop's resources your product consumes (machine time, labor hours, floor space), the larger its share of the overhead bill. Getting that split right is what overhead allocation is all about.

📐 Browse all 1000+ Interactive Calculators

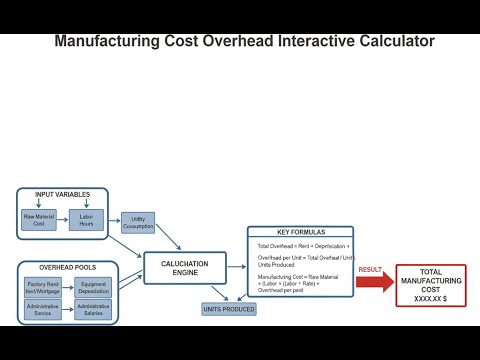

Visual Diagram: Manufacturing Cost Structure

Manufacturing Cost Overhead Calculator

How to Use This Calculator

- Select your Calculation Mode from the dropdown — choose from overhead rate, total cost, unit cost, required overhead budget, allocation base, or cost breakdown analysis.

- Enter the relevant cost inputs that appear for your selected mode — this may include total overhead costs, direct materials, direct labor, allocation base, units produced, or target overhead rate.

- Double-check your figures against your actual cost data or budget estimates before calculating.

- Click Calculate to see your result.

Manufacturing Cost Overhead Interactive Visualizer

Watch how overhead allocation affects your total manufacturing cost in real-time. Adjust materials, labor, overhead, and production volume to see immediate impact on unit cost and profitability.

OVERHEAD RATE

200%

TOTAL MFG COST

$105K

UNIT COST

$52.50

FIRGELLI Automations — Interactive Engineering Calculators

Formulas & Equations

Overhead Rate Formula

Use the formula below to calculate the overhead rate.

Overhead Rate (%) = (Total Overhead Costs / Allocation Base) × 100

Where:

- Total Overhead Costs = Sum of all indirect manufacturing costs (dollars)

- Allocation Base = Direct labor cost, machine hours cost, or other activity base (dollars or dollars equivalent)

- Overhead Rate = Percentage applied per dollar of allocation base (%)

Total Manufacturing Cost Formula

Use the formula below to calculate total manufacturing cost.

Total Cost = Direct Materials + Direct Labor + Manufacturing Overhead

Where:

- Direct Materials = Raw materials directly traceable to products (dollars)

- Direct Labor = Labor directly traceable to production (dollars)

- Manufacturing Overhead = Indirect factory costs (dollars)

Unit Cost Formula

Use the formula below to calculate unit cost.

Unit Cost = Total Manufacturing Cost / Units Produced

Where:

- Unit Cost = Cost per individual unit (dollars per unit)

- Total Manufacturing Cost = Sum of all product costs (dollars)

- Units Produced = Number of finished goods units (units)

Prime Cost and Conversion Cost Formulas

Use the formula below to calculate prime cost and conversion cost.

Prime Cost = Direct Materials + Direct Labor

Conversion Cost = Direct Labor + Manufacturing Overhead

Where:

- Prime Cost = Total direct costs of production (dollars)

- Conversion Cost = Cost to convert materials into finished goods (dollars)

Applied Overhead Formula

Use the formula below to calculate applied overhead.

Applied Overhead = Predetermined Overhead Rate × Actual Allocation Base

Where:

- Applied Overhead = Overhead assigned to production (dollars)

- Predetermined Overhead Rate = Overhead rate calculated before period begins (decimal or %)

- Actual Allocation Base = Actual activity level during period (dollars or hours)

Simple Example

A small machining shop has $50,000 in total overhead and $100,000 in direct labor cost for the month. They produce 2,000 units using $30,000 in materials and $20,000 in direct labor.

- Overhead Rate = ($50,000 / $100,000) × 100 = 50%

- Total Manufacturing Cost = $30,000 + $20,000 + $50,000 = $100,000

- Unit Cost = $100,000 / 2,000 = $50.00 per unit

Theory & Engineering Applications

Manufacturing overhead represents the third critical component of product costing, alongside direct materials and direct labor. Unlike these direct costs that can be traced to specific products with precision, overhead encompasses all indirect factory costs—from depreciation on production equipment and factory utilities to quality control salaries, maintenance supplies, and factory insurance. The fundamental challenge in overhead accounting is not simply tracking these costs, but developing systematic methods to allocate them fairly and accurately across diverse products with different resource consumption patterns.

The Architecture of Manufacturing Overhead

Manufacturing overhead divides into three practical categories that guide allocation strategy. Fixed overhead remains constant regardless of production volume—annual depreciation on a $2 million injection molding machine continues whether the facility produces 10,000 units or 100,000 units. Variable overhead scales proportionally with activity—if electricity consumption averages $0.12 per machine hour, doubling production hours doubles energy costs. Semi-variable overhead contains both fixed and variable components—a maintenance department requires core staff (fixed) plus additional technicians and supplies during high-volume periods (variable).

This distinction matters profoundly for decision-making. A production manager evaluating whether to accept a special order at $47 per unit must know that while variable overhead will increase by $3.80 per unit, the $127,000 in monthly fixed overhead remains unchanged. The incremental cost analysis requires isolating variable overhead from the total overhead pool. Many manufacturing operations struggle with this separation because accounting systems aggregate overhead into single line items, obscuring the fixed-variable behavior that drives marginal analysis.

Allocation Base Selection: Beyond Direct Labor Hours

Traditional overhead allocation used direct labor hours or direct labor cost as the allocation base, reflecting manufacturing environments where labor-intensive assembly dominated production. A furniture manufacturer spending $450,000 annually on direct labor and $225,000 on overhead would calculate a 50% overhead rate, applying $0.50 of overhead for every dollar of direct labor. This approach worked reasonably well when labor represented the primary cost driver and products consumed overhead in proportion to labor content.

Modern manufacturing has inverted this relationship. In automated facilities, direct labor may represent only 5-12% of total cost while overhead—driven by expensive equipment, sophisticated process control systems, and automated material handling—dominates the cost structure. Consider a precision machining operation where a five-axis CNC milling center with $847,000 in annual depreciation and operating costs produces components requiring only 18 minutes of direct operator supervision per part. Allocating this equipment's overhead based on minimal labor hours grotesquely distorts product costs.

Activity-based costing (ABC) emerged to address this distortion by identifying multiple cost drivers. Machine hours become the allocation base for equipment depreciation and energy costs. Material handling costs allocate based on number of components or material movements. Setup costs allocate based on production runs. Quality inspection costs allocate based on inspection points. A plastic injection molding facility might use machine hours for press depreciation and energy ($438 per hour), setup hours for changeover costs ($285 per setup), and pounds of resin for material handling ($0.17 per pound). This multi-driver approach reveals that simple products with high volume absorb less overhead per unit than complex, low-volume products requiring frequent setups and specialized handling.

The Predetermined Rate Challenge and Variance Analysis

Manufacturers calculate overhead rates before the fiscal period begins because actual overhead and actual allocation base levels are unknown until year-end. A fabrication shop estimates $1,850,000 in annual overhead and 37,000 machine hours, yielding a predetermined rate of $50 per machine hour. Throughout the year, jobs consume overhead at this $50 rate. The accounting system debits Work-in-Process inventory for applied overhead as production occurs.

At year-end, the shop discovers actual overhead totaled $1,923,000 and actual machine hours reached 38,200. Applied overhead equals $50 × 38,200 = $1,910,000, creating a $13,000 underapplied overhead variance ($1,923,000 actual minus $1,910,000 applied). This variance decomposes into two components: the spending variance reflects actual costs exceeding budgeted costs at the actual activity level, while the volume variance captures the fixed overhead allocation error from producing more or fewer units than anticipated. The shop must close this variance to Cost of Goods Sold or allocate it proportionally across inventory accounts, affecting profitability reporting and inventory valuation.

Variance analysis extends beyond simple reconciliation to strategic insight. Persistent overapplied overhead (applied exceeds actual) suggests rates are too high, potentially making bids uncompetitive. Persistent underapplied overhead indicates underestimated rates, threatening profitability when fixed-price contracts lock in selling prices based on understated costs. Monthly variance tracking enables mid-year rate adjustments, preventing large year-end surprises. A medical device manufacturer discovering 15% underapplied overhead after six months should immediately reassess its $127 per direct labor hour rate for remaining production.

Advanced Allocation: Department Rates and Service Department Allocation

Multi-departmental facilities often require department-specific overhead rates because different production departments consume overhead at dramatically different rates. An electronics assembly plant's surface mount technology (SMT) department operates $4.3 million in automated placement equipment, generating $820,000 in annual overhead from 14,000 machine hours—yielding $58.57 per machine hour. The wave soldering department uses $340,000 in overhead across 22,000 direct labor hours—yielding $15.45 per labor hour. The final assembly department incurs $185,000 overhead across 28,000 labor hours—yielding $6.61 per labor hour. A single plant-wide rate would average these to perhaps $31 per labor hour, dramatically overcosting labor-intensive products and undercosting machine-intensive products.

Service department allocation adds another layer of complexity. Maintenance, quality assurance, and material handling departments don't directly produce goods but support production departments. Their costs must be allocated to production departments before calculating final overhead rates. The direct method allocates service department costs directly to production departments, ignoring inter-service-department support. The step-down method allocates in sequence, recognizing one-way inter-service support. The reciprocal method uses simultaneous equations to fully recognize mutual inter-service support. A facility with $280,000 in maintenance costs (serving all departments) and $165,000 in quality costs (serving production only) will generate different production department rates depending on allocation method—impacting product costs by 3-7% in complex plants.

Worked Example: Multi-Mode Overhead Analysis

Consider Precision Components Inc., a contract manufacturer producing machined aerospace parts. The company faces several overhead decisions simultaneously:

Given Data:

- Annual overhead costs: $2,847,000

- Expected machine hours: 47,000 hours

- Direct materials cost for Job 2847: $16,340

- Direct labor cost for Job 2847: $8,720

- Machine hours for Job 2847: 127 hours

- Units produced in Job 2847: 850 units

- Target profit margin: 22% on total cost

Step 1: Calculate predetermined overhead rate

Overhead Rate = $2,847,000 ÷ 47,000 hours = $60.574 per machine hour

The company will apply $60.574 of overhead for each machine hour consumed by production jobs.

Step 2: Calculate applied overhead for Job 2847

Applied Overhead = $60.574/hour × 127 hours = $7,692.90

This specific job will absorb $7,692.90 in overhead costs based on its 127-hour machine time consumption.

Step 3: Calculate total manufacturing cost for Job 2847

Total Cost = $16,340 (DM) + $8,720 (DL) + $7,692.90 (OH) = $32,752.90

Prime Cost (DM + DL) = $16,340 + $8,720 = $25,060 (76.5% of total cost)

Conversion Cost (DL + OH) = $8,720 + $7,692.90 = $16,412.90 (50.1% of total cost)

Step 4: Calculate unit cost

Unit Cost = $32,752.90 ÷ 850 units = $38.533 per unit

Breaking down per-unit costs: Materials = $19.224, Labor = $10.259, Overhead = $9.050

Step 5: Determine required selling price

To achieve 22% profit margin on total cost: Required Selling Price = $32,752.90 × 1.22 = $39,958.54

Per unit selling price = $39,958.54 ÷ 850 = $47.01 per unit

This price structure allocates $10.48 per unit to profit, covering overhead allocation and providing target return.

Step 6: Analyze cost structure implications

Overhead represents 23.5% of total manufacturing cost for this job. The relatively balanced structure (materials 49.9%, labor 26.6%, overhead 23.5%) suggests appropriate complexity for the product. If overhead exceeded 40%, management should investigate whether machine-intensive jobs are absorbing disproportionate facility costs. If overhead fell below 15%, the predetermined rate may be inadequate, risking underapplied overhead at year-end.

Step 7: Sensitivity analysis on machine hours

If engineering can reduce machine time by 15% through tooling improvements (127 → 108 hours), overhead drops to $6,541.99, reducing total cost to $31,601.99 and unit cost to $37.18. At the same $47.01 selling price, profit margin increases from 22% to 26.4%. This $1.35 unit cost reduction directly improves competitiveness in bid situations where customers compare quotes from multiple manufacturers.

Strategic Applications in Manufacturing Decision-Making

Overhead analysis drives make-or-buy decisions with profound strategic implications. A manufacturer considering outsourcing a component currently produced in-house must separate avoidable overhead (variable overhead that disappears if production stops) from unavoidable overhead (fixed costs continuing regardless of the outsourcing decision). If in-house production costs $23.50 per unit with $8.70 in overhead, but $5.30 of that overhead is fixed facility cost continuing even if outsourced, the relevant comparison cost is only $18.20. An outsource quote of $21.00 appears $2.50 cheaper than the $23.50 full cost, but actually costs $2.80 more than the $18.20 avoidable cost.

Capacity utilization decisions similarly hinge on overhead behavior. A facility operating at 65% capacity with $1.2 million in fixed overhead spreads that cost over fewer units, inflating unit costs. Accepting lower-margin work to boost utilization to 85% doesn't reduce fixed overhead, but spreads it over more units, reducing per-unit burden. If fixed overhead per unit drops from $14.80 to $11.35 through volume increase, products can be repriced more competitively while maintaining or improving absolute profit dollars. This explains why manufacturers often pursue "capacity-filling" business at margins below standard product margins—the incremental contribution exceeds the truly incremental (variable) overhead cost.

Process improvement initiatives must account for overhead impacts beyond direct labor savings. Automating an assembly operation might eliminate $180,000 in direct labor but add $340,000 in annual equipment depreciation and maintenance overhead. The business case depends on material yield improvements, quality enhancements, and throughput increases that aren't captured in simple labor cost analysis. A manufacturer producing 450,000 units annually saves $0.40 per unit in direct labor but adds $0.76 per unit in overhead—a net $0.36 cost increase.

However, if automation also reduces defects from 3.2% to 0.8%, the $0.40 per unit savings in rework and scrap tips the analysis strongly positive. Comprehensive overhead modeling prevents the common mistake of automating operations where the fully-loaded automation overhead exceeds the direct labor saved.

For additional manufacturing cost analysis tools and engineering calculators, visit the FIRGELLI Engineering Calculator Hub.

Practical Applications

Scenario: Medical Device Manufacturing Cost Analysis

Dr. Emily Rodriguez, a manufacturing engineer at a medical device startup, is preparing a cost model for FDA submissions and investor presentations for their new implantable sensor. The regulatory filing requires detailed cost breakdowns demonstrating manufacturing feasibility. With $487,000 in annual cleanroom facility overhead, $156,000 in specialized equipment depreciation, and $89,000 in quality and compliance overhead—totaling $732,000 overhead against an allocation base of $915,000 in direct labor—she uses this calculator to determine their 80.0% overhead rate. For the first production lot of 2,400 sensors with $68,400 in materials and $51,200 in direct labor, applied overhead reaches $40,960, yielding a total unit cost of $66.90. This detailed costing supports her target selling price of $127 per unit to distributors, demonstrating sustainable 47% gross margins that satisfy both FDA manufacturing capability requirements and venture capital return expectations.

Scenario: Custom Furniture Shop Bid Preparation

Marcus Chen operates a custom furniture fabrication shop specializing in commercial installations for restaurants and hotels. When preparing a bid for 45 restaurant tables requiring $12,870 in hardwood materials and 340 hours of skilled labor at $32/hour ($10,880 total labor), he needs to accurately allocate his $187,000 annual overhead across this project. Using the calculator's allocation base mode with his total annual direct labor budget of $374,000, he calculates a 50% overhead rate, adding $5,440 in overhead to this job. The total cost of $29,190 divided by 45 tables yields $648.67 per table. Marcus adds his standard 35% markup, arriving at a bid price of $875.70 per table ($39,407 total project). This systematic overhead allocation ensures he covers his shop rent, equipment maintenance, utilities, and insurance while remaining competitive against three other bidders. The calculator helped him avoid the common small-business mistake of underpricing by forgetting to allocate overhead proportionally across all jobs.

Scenario: High-Volume Electronics Assembly Optimization

Jennifer Park, operations manager at a contract electronics manufacturer, is evaluating whether to invest $680,000 in additional surface-mount technology (SMT) equipment to reduce outsourcing. Her current operation runs $2.34 million in annual overhead across 52,000 machine hours (current rate: $45.00/hour). The new equipment would add $127,000 in annual depreciation and operating overhead but enable 12,000 additional machine hours annually. Using the calculator, she models the new scenario: $2,467,000 overhead ÷ 64,000 hours = $38.55/hour, an overhead rate reduction of 14.3%. For her typical product mix of 280,000 assemblies annually consuming 1.3 hours average machine time, this rate reduction saves $23.66 per assembly ($6.63 million annual savings). Even after accounting for the $127,000 additional overhead, the capacity expansion generates positive ROI within 11 months while bringing previously outsourced volume in-house. The cost breakdown analysis mode reveals overhead will drop from 42% to 37% of total manufacturing cost, significantly improving competitive positioning in price-sensitive consumer electronics markets.

Frequently Asked Questions

What's the difference between manufacturing overhead and administrative overhead? +

Why do my actual overhead costs differ from applied overhead at year-end? +

Should I use direct labor hours or machine hours as my allocation base? +

How does overhead allocation affect make-or-buy decisions? +

What overhead rate is considered normal or typical for manufacturing? +

How frequently should I recalculate my predetermined overhead rate? +

Free Engineering Calculators

Explore our complete library of free engineering and physics calculators.

Browse All Calculators →🔗 Explore More Free Engineering Calculators

About the Author

Robbie Dickson — Chief Engineer & Founder, FIRGELLI Automations

Robbie Dickson brings over two decades of engineering expertise to FIRGELLI Automations. With a distinguished career at Rolls-Royce, BMW, and Ford, he has deep expertise in mechanical systems, actuator technology, and precision engineering.

Need to implement these calculations?

Explore the precision-engineered motion control solutions used by top engineers.